Step-By-Step Instructions For Filing Form 1099-NEC

Partnering with vendors is an important part of being a small business owner. One aspect of working with vendors is making sure you’re complying with applicable state and federal tax rules.

Similar to employees having a set of tax rules that business owners must follow, vendors have their own set of rules that owners are responsible for.

One of these rules is how payments to certain vendors are reported to the IRS. This article takes a look at one of the most common tax forms when it comes to reporting vendor payments, Form 1099-NEC.

What Is Form 1099-NEC?

Business owners file Form 1099-NEC with the IRS to report payments made by businesses to certain vendors, freelancers, contractors, sole proprietors, and other self-employed workers.

The acronym “NEC” stands for “Nonemployee Compensation” and means exactly what it sounds like. While Form W-2 is provided to full-time and part-time employees to report, Form 1099-NEC is provided to “nonemployees”, otherwise known as vendors and/or contractors.

How is Form 1099-NEC different from Form 1099-MISC?

There are more than a dozen different types of Form 1099s. But the two types you will probably encounter the most are Form 1099-NEC and Form 1099-MISC.

Businesses used to report nonemployee compensation on Form 1099-MISC. Starting with the 2020 tax year, the IRS began requiring nonemployee compensation be reported on its own form, Form 1099-NEC.

Form 1099-MISC is still used to report the following types of payments:

Rents of $600 or more

Royalties of $10 or more

Gross proceeds paid to an attorney (for example, percent of settlement; attorneys’ fees are reported on Form 1099-NEC) of $600 or more

Crop insurance proceeds of $600 or more

Excess golden parachute payments

Fishing boat proceeds (for an individual’s share of the catch)

Fish purchases for cash (when purchasing fish for resale) of $600 or more

Payments of $600 or more paid to each physician or other supplier or provider of medical or health care services.

Click here to learn more about Form 1099-MISC and other 1099s.

Other types of 1099s you may receive as a business include:

Form 1099-K: Reports payments received from customers through a third-party payment processor, such as a credit card company or an online platform such as PayPal.

Form 1099-B: Reports proceeds received from broker and barter exchange transactions. It contains information about stocks, mutual funds, bonds, and other securities.

The IRS is so serious about businesses filing all required types of 1099s that each type of business tax return — Schedule C on Form 1040 for sole proprietors, Form 1065 for partnerships, Form 1120-S for S corporations, and Form 1120 for C corporations — has the following two questions about 1099s that you MUST answer:

Did you make any payments in 2023 that would require you to file Form(s) 1099? (Check ‘Yes’ or ‘No’)

If “Yes,” did you or will you file required Form(s) 1099?

Who Files Form 1099-NEC?

You’ll need to file Form 1099-NEC for each person you paid at least $600 during the course of a tax year in the following scenarios:

Services performed by someone who is not your employee.

Fees paid to an attorney.

To report sales totaling $5,000 or more of consumer products to a person on a buy-sell, a deposit-commission, or other commission basis for resale.

For each person from whom you have withheld any federal income tax under the backup withholding rules, regardless of the amount of the payment.

You only need to report each payment that was made in the course of your trade or business. Personal payments are not reportable.

Corporations, including C corporations and S corporations, typically aren’t required to receive a 1099 for payments you make to them because they’re considered separate legal entities. All other non-corporate entities, including individuals and partnerships, should receive a 1099 if you made payments to them during the tax year in question.

Another way to look at this question…you’ll only issue a Form 1099 for services rendered by an individual, not for receiving a product.

Form 1099-NEC Filing Instructions

You’ll need the following information to properly prepare a Form 1099-NEC:

Payer information (this is your business), including your name, address, and Taxpayer Identification Number (this can be your Social Security number).

Recipient information, including their name, address, and Taxpayer Identification Number (this can also be a Social Security number).

Payment information. Provide the total amount paid to the recipient during the tax year in question in Box 1. Record total Federal income tax withheld, if any, in Box 4.

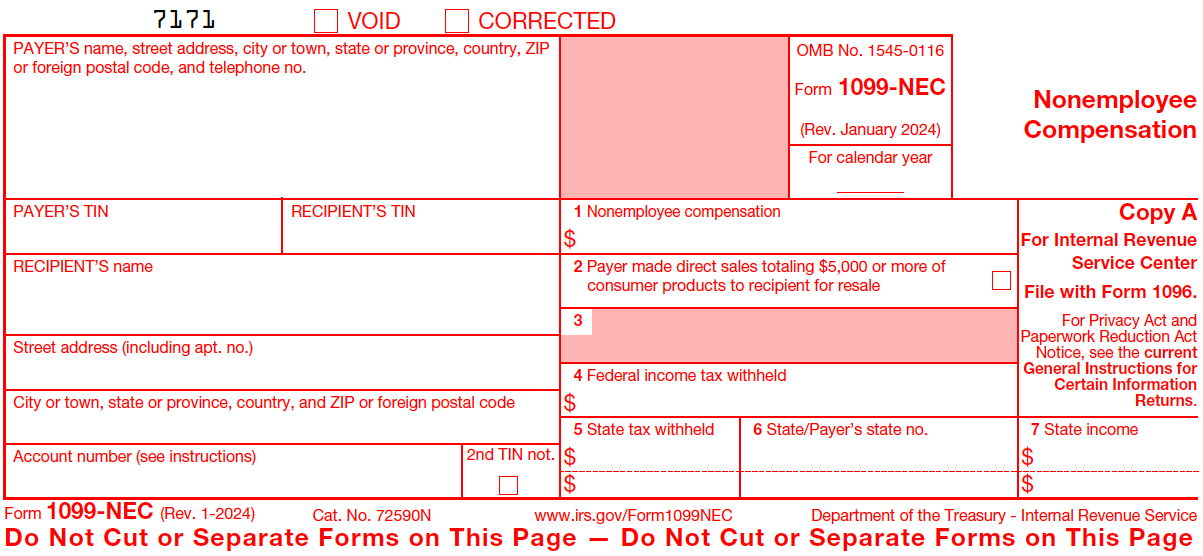

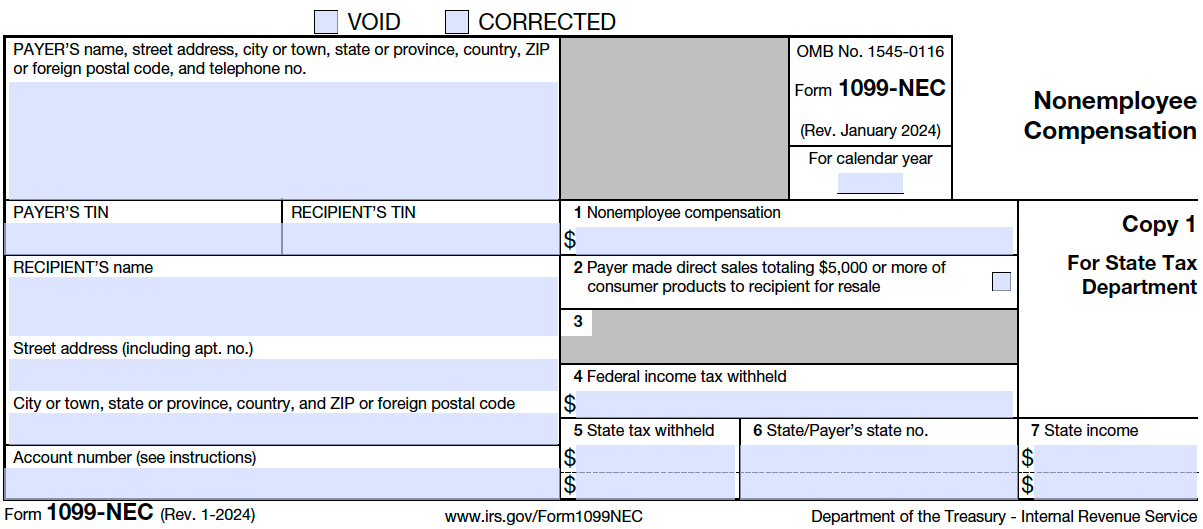

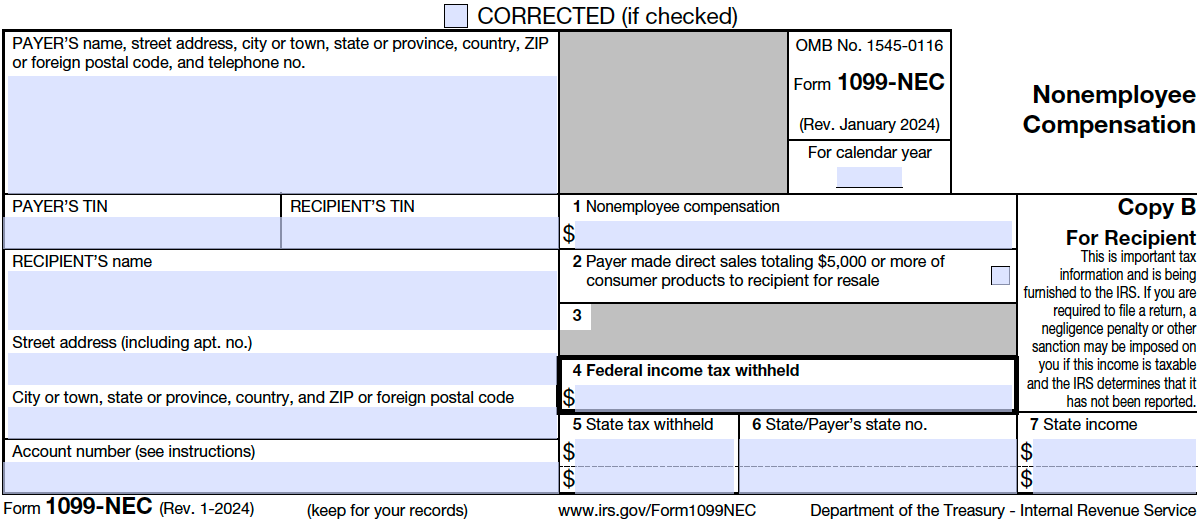

There are 3 different copies of Form 1099-NEC:

Copy A is filed with the Internal Revenue Service.

Copy 1 is filed, if applicable, with the state tax department.

Copy B is provided to the recipient.

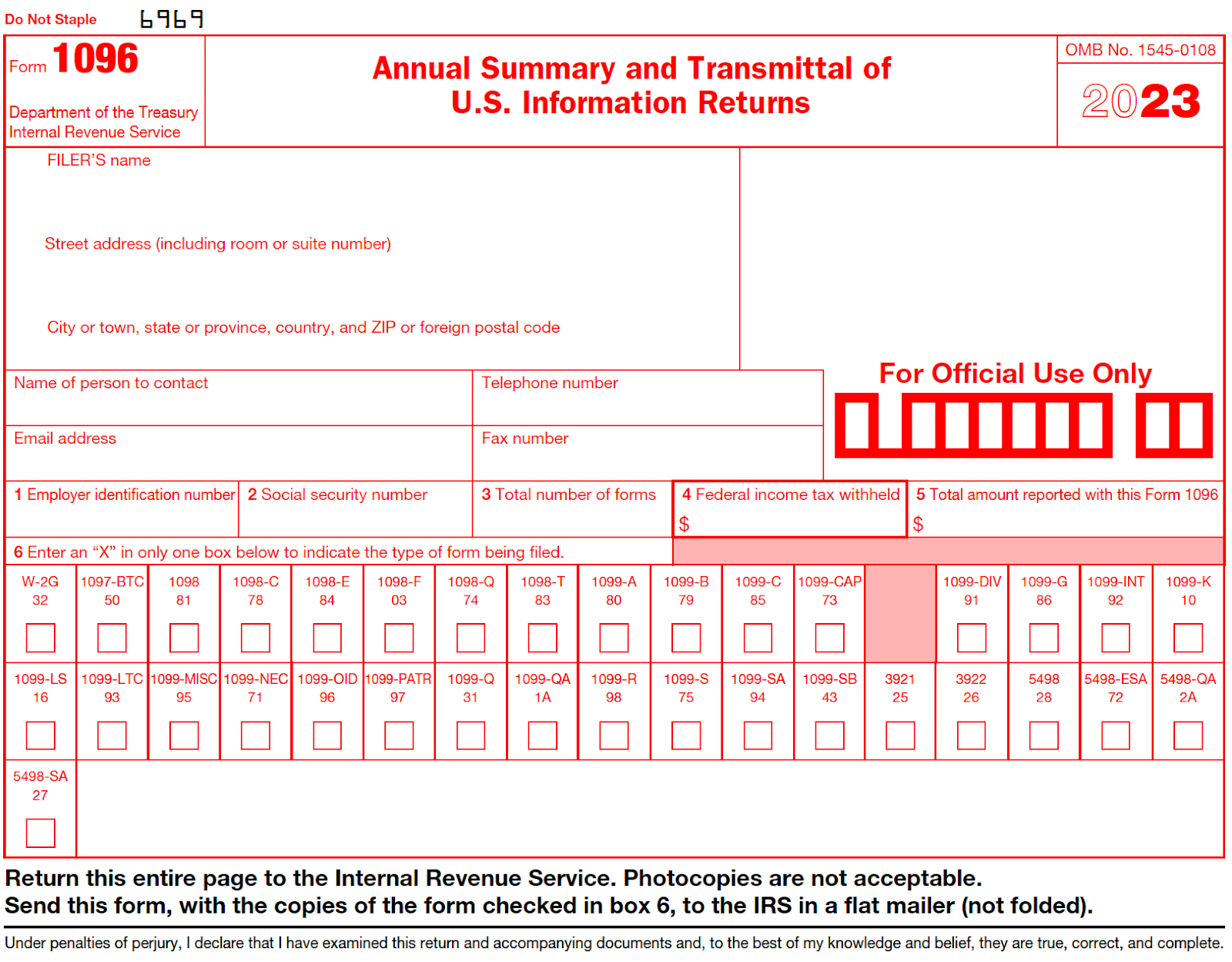

The final step is to prepare and file Form 1096. This form is a summary of all your Form 1099-NECs, and should be filed in conjunction with all your prepared 1099-NECs. Be sure that the total dollar amount on Form 1096 agrees with the combined total of all your 1099-NECs.

NOTE: You must include a separate Form 1096 for each type of Form 1099 submitted. For example, DO NOT mix together Form 1099-NECs with Form 1099-MISCs.

Form 1099-NEC: Penalties For Late Filing

The due date to file Form 1099-NEC is January 31st (or the following business day if January 31st falls on a weekend).

One 30-day extension may be granted by filing a signed Form 8809, though an explanation may be required for the extension. Under certain hardship conditions, you may apply for an additional 30-day extension.

You may be subject to the following fines and penalties if you’re late filing Form 1099-NEC:

$60 per form if properly and accurately filed within 30 days of the due date. The maximum penalty is $232,500 for small businesses and $664,500 for large businesses.

$130 per form if properly and accurately filed more than 30 days after the due date but by August 1. The maximum penalty is $664,500 for small businesses and $1,993,500 for large businesses.

$330 per form if filed after August 1 or if corrections are not filed. The maximum penalty is $1,329,000 for small businesses and $3,987,000 for large businesses.

$660 per form with no maximum penalty for intentional disregard.

NOTE: For purposes of the lower maximum penalties, a small business is defined as having average annual gross receipts of $5 million or less for the 3 most recent tax years.

The best way to avoid these fines and penalties is to file your Form 1099-NECs (and all other Form 1099s and tax forms) on time. And the best way to ensure that you file your forms on time is to have a great bookkeeping system in place and up-to-date.

How bookkeeping can help avoid Form 1099-NEC headaches

It can be confusing to know which of your contractors and vendors need a Form 1099-NEC from you. It can be that much more stressful if the January 31st deadline for filing Form 1099-NEC is slowly approaching and you realize that you don’t know the total amount of payments to each vendor your bookkeeping isn’t up-to-date.

Timely and accurate bookkeeping can help you prepare your required Form 1099s, and all other required 1099s and tax forms, on time by having the necessary payment information accurately entered when the transaction occurs.

One way to make sure you never fall behind on your bookkeeping and tax filings is by partnering with 1-800Accountant’s bookkeeping service. Schedule a free call today to find out how your essential tax filings and bookkeeping can be taken care of by a small business-focused tax service.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult his or her own attorney, business advisor, or tax advisor with respect to matters referenced in this post. 1‑800Accountant assumes no liability for actions taken in reliance upon the information contained herein.